.png)

Accounting firms pride themselves on being both efficient and precise in their work. Yet when it comes to tax research, many firms are quietly bleeding money. Multiple legacy tax research tools remain on the books even as adoption rates continue to fall, creating a layer of underused software that eats into budgets without improving outcomes.

For numbers-savvy accounting firms, cutting these underused tools in favour of more user-friendly alternatives like AI-powered tax research solutions seems like the obvious choice. But their real-world behavior isn’t always so logical. Perceived value, sunk costs, and status quo comfort keep legacy tax research platforms in play. The result is wasted spend and a missed opportunity to gain easier access to better tax answers.

In this article, you’ll find the following:

- Data on the underuse of legacy tax research platforms

- Insights into which other tools tax practitioners are using for research

- A formula to calculate the true cost of the access-adoption gap

- A breakdown of the factors that keep firms tied to legacy tools

- Practical advice to overcome legacy tool inertia

The Gap Between Licenses and Logins

Earlier this year, Blue J and CPA.com surveyed 150+ tax practitioners to gain insights into how firms approach tax research. The result is the AI Tax Research Solution Outlook Report. The data in this report reveals a consistent trend of poor adoption for a certain class of tax research tools.

- On average, respondents reported having access to three tax research solutions. However, they only reported using two of these three tools on a daily or weekly basis.

- Among respondents who use legacy tax research tools, adoption rates are consistently lower than for other classes of solutions.

When speaking with leaders from mid-to-large accounting firms specifically, the adoption rates for legacy tools typically sit at 15%-25%. Comparing these adoption rates to those seen in Blue J’s user data—with 75%+ of users logging in monthly—there’s a clear gap between how much firms use legacy tools versus their AI-powered counterparts.

Looking Elsewhere For Tax Answers

But even with multiple tax research tools at their fingertips, tax and accounting professionals aren’t always turning to them for answers. As it turns out, many tax practitioners are instead choosing the speed and familiarity of search engines or experimenting with general-purpose AI tools to find answers to their tax questions.

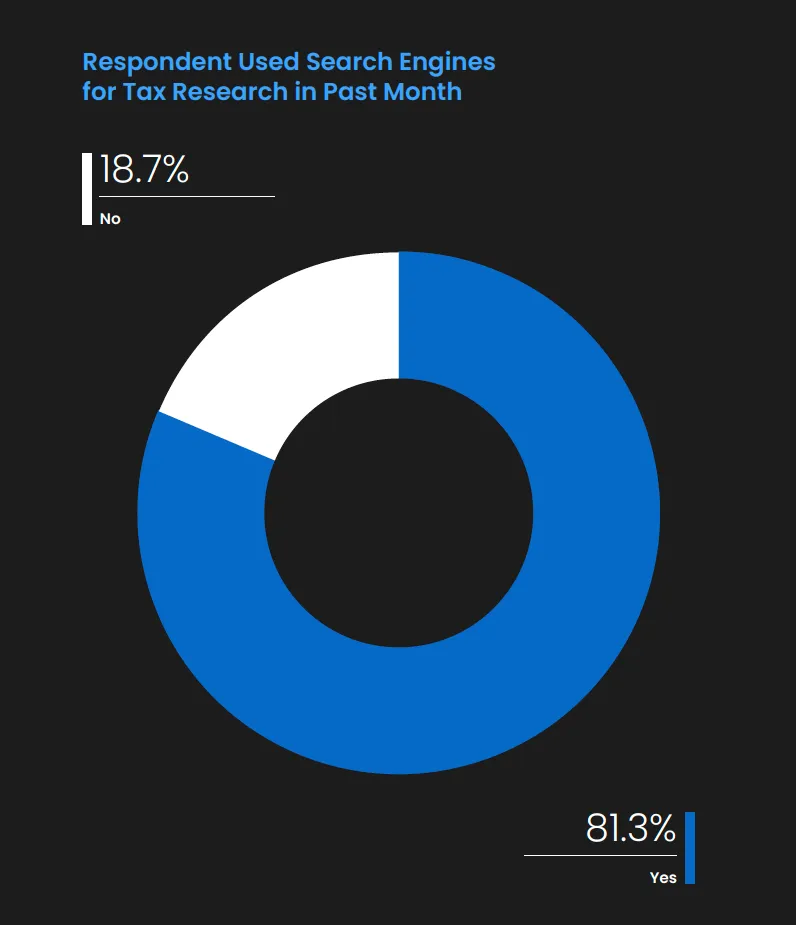

Blue J’s Outlook Report revealed that 81.3% of tax professionals use search engines such as Google to perform tax research.

This finding isn’t surprising when you consider the familiarity and ease of typing a question into a search engine. This makes it a natural starting point when more specialized tools are time-consuming to use, hard to navigate, and lacking key functionality—all top complaints of legacy tax research tool users.

AI is an attractive alternative

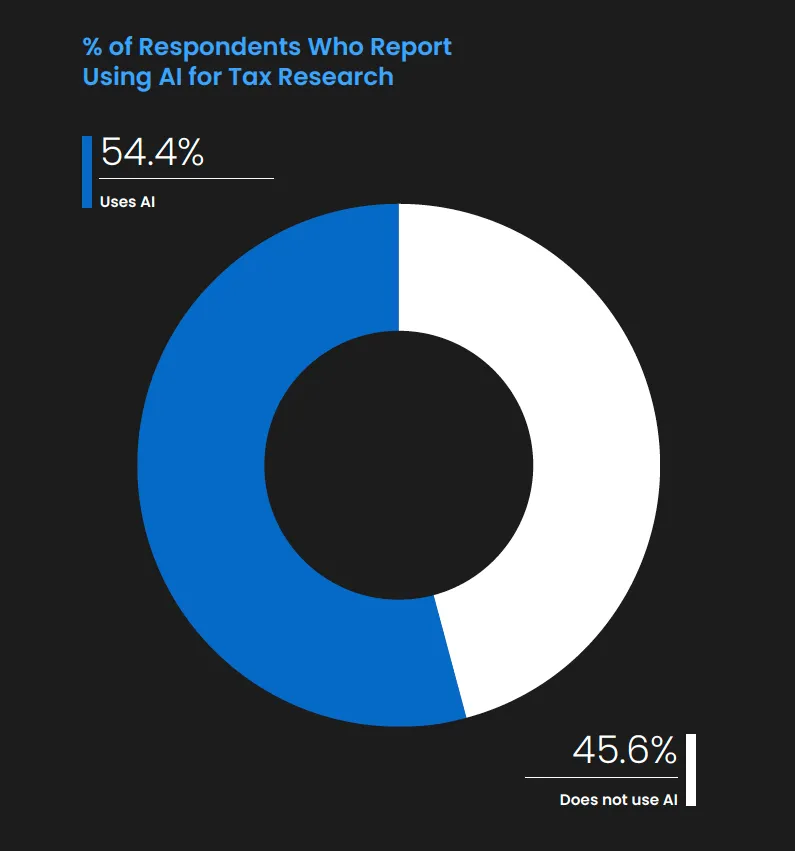

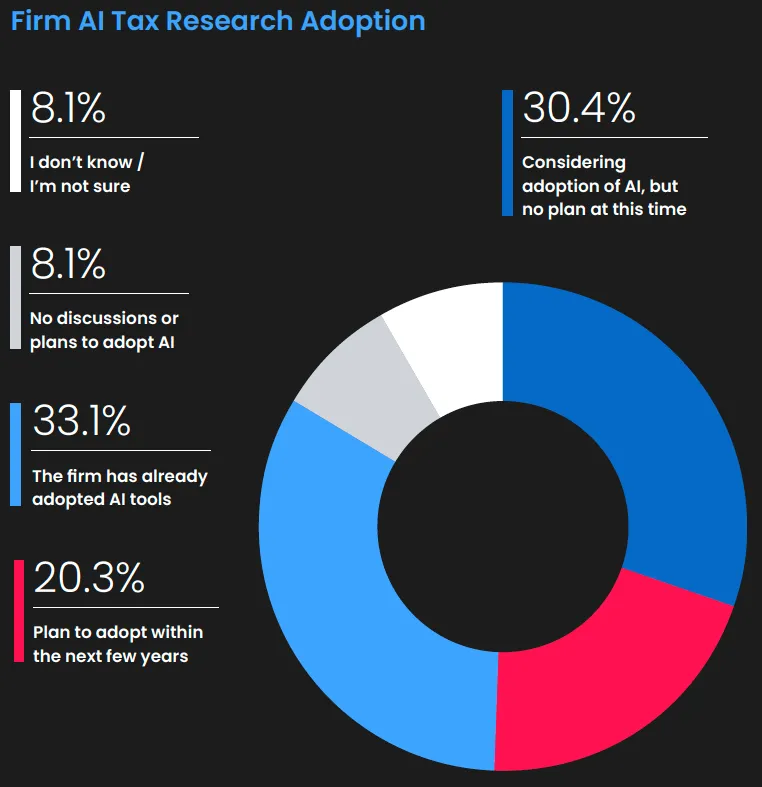

Search engines aren’t the only alternatives tax practitioners are turning to for answers. Our Outlook Report also uncovered a discrepancy between the number of respondents who report using AI for tax research (54.4%) and the percentage who work for firms that have formally adopted AI-supported tools (33.1%).

This gap points to unsanctioned AI use, where individuals may be leveraging general-purpose AI tools to perform tax research—without their firm’s knowledge.

Similar to search engines, AI adoption parallels real-life behaviors. As people become increasingly comfortable using AI in their day-to-day lives, that behavior can then easily translate into their work. A paper published collaboratively by OpenAI, Duke University, and Harvard University reports that 18 billion messages were sent each week by 700 million users on ChatGPT as of July 2025. The popular AI tool achieved this growth less than three years after launching, in what’s been a meteoric rise towards mass adoption.

People are now as comfortable asking questions of AI tools as they are typing them into Google. In the case of tax research, this comfort with both search engines and general-purpose AI tools raises challenges for firms.

Unsanctioned research tools introduce risk

While general-purpose AI tools and search engines are easy to incorporate into research workflows, the efficiency they offer often comes at the expense of answer accuracy. For general-purpose AI tools, this issue is more acute as answers are presented in a cohesive way that can make them seem more convincing, all the while:

- These tools pull from a wide range of uncurated sources, making them prone to error.

- Answers are often based on irrelevant and outdated sources, which can be difficult and time-consuming to verify.

- General-purpose AI tools lack tax specialization, missing out on the accuracy benefits that come from human-in-the-loop approaches, user verification of outputs, and tax research-tuned algorithms.

Outside of accuracy concerns, client security and privacy can also become an issue for both search engines and general-purpose AI tools. Not only do most lack the security measures expected of tax practitioners to adequately protect sensitive client information, but certain AI tools even use information submitted by users to train their models.

The irony is that even while firms may be aware of the risks of staff turning to search engines or general-purpose AI tools, they still choose to pay for legacy tax research tools their teams don’t use. When team members aren’t getting the experience they want from legacy tools, firms can’t be surprised when they turn to alternative options instead. Between inaccurate answers and unused subscriptions, the costs add up quickly.

Calculating the High Cost of Low Adoption

Paying for access to legacy tools doesn’t mean you’re getting their full value. The real cost driver isn’t license fees, it’s adoption. For example, if a firm pays for 200 seats, but only a fifth of those licenses get used, the effective cost per active user is high.

Our Outlook Report revealed that AI-powered research tools, like Blue J, enjoy significantly higher adoption rates. Even at the same total license spend, the cost per active user plummets, meaning firms get more value from the tools they’re paying for.

You can start to understand what this value looks like by calculating the cost per active user. The formula to determine this cost is simple:

(Total cost for all licenses) ÷ # of active users = Cost per active user

To contextualize this calculation, let’s go back to those specific adoption rates we discussed earlier. Doing so, you can get a better idea of just how vast this difference in value can be.

- 15%-25% adoption rate for legacy tax research tools within mid-to-large firms.

- 75%+ monthly active usage for comparable firms using Blue J.

To start with this first rate, imagine a firm purchases 200 seats at $1,500 each for a total cost of $300,000. If only 20% of users are active, the effective cost per active user is $7,500—not $1,500.

($300,000) ÷ 40 active users = $7500 per active user

By comparison, a firm spending the same on total license costs with 75% of users active would see a much lower cost per active user.

($300,000) ÷ 150 active users = $2000 per active user

Once you crunch the numbers, the savings are black and white. It begs the question: why do firms keep paying for unused licenses?

Why Firms Keep Paying for Legacy Tools (Despite Low Adoption)

A mix of perceived value, vendor lock-in, and cognitive bias keeps legacy tools on the books even when staff aren’t using them.

- Proprietary content: Legacy platforms offer access to content that feels essential, primarily proprietary editorial commentary. There may be comfort in knowing that content is available, even if team members can’t easily navigate the library to find the sources they need.

- Sunk cost fallacy: The sunk cost fallacy is a cognitive bias where past investment convinces people to stick with failing options. After years of spending on licenses, training, and integrations, firms may keep renewing legacy tools simply because they’ve already poured money and time into them. Short of legacy systems causing an obvious crisis, the sunk cost fallacy unconsciously promotes inaction.

- Perceived credibility: Legacy tax research tool vendors also benefit from well-established brand authority. The narrative that a solution from a legacy vendor is defensible is a powerful one, even when the day-to-day experience is bad enough to deter most team members from actually using it.

- Incumbent advantage: Legacy tools are already embedded in firm workflows. Vendors then expand their footprint with deeply discounted product add-ons, which makes staying put feel easier and lower cost in the short term. But even when AI-powered research add-ons are incorporated to counteract navigation issues, they often fail to measure up to their AI-first counterparts on answer accuracy.

- Change management friction: Switching requires first unwinding long-term, often bundled contracts, followed by training staff, revising processes, and updating internal templates or workflows. While worries about the pain of winding down are valid, the ramp-up for AI-powered tools is often far easier than firms expect. For Blue J users, it typically takes only 2.8 minutes after logging in for the first time to generate a comprehensive tax answer.

- Cultural dynamics: Firm leaders may not want to be the ones who “take away” a long-standing tool (even if usage is low) because they risk internal pushback. Senior partners who built their careers using these legacy tax research tools have mastered clunky Boolean and keyword searches. They may feel uneasy walking away from them, even when younger staff are eager to use AI-powered alternatives.

Despite all the reasons firms have for sticking with legacy tax research tools, the cracks are showing. Tightening budgets and rising client expectations are both putting pressure on teams. Facing these forces, unused tools that send teams to unreliable alternatives are no longer an ignorable issue.

Pressure to change

With the adoption of generative AI accelerating across industries, it’s only natural for accounting to follow suit. Blue J’s own user data shows this shift clearly: between July 2024 and July 2025, our generative AI solution for tax research logged a +735% increase in questions asked YoY.

Firms are also feeling internal pressure to evolve. Blue J customer, Bartlett, Pringle, and Wolf, LLP (BPW), recently shared their story of adopting AI for tax research. Senior partners at the firm observed that juniors were increasingly graduating well-versed in using generative AI. It became clear that not offering staff an AI solution was negatively impacting recruitment.

Today, staff across all levels of seniority at BPW use Blue J for tax research. Officially sanctioning an AI-powered tax research tool wasn’t just about efficiency. It was about letting go of legacy mindsets and aligning technology with how the next generation of professionals expects to work.

From Legacy Adoption Gaps to AI Growth. What’s Next?

It’s already happening. Tax practitioners are turning to generative AI for tax research—regardless of whether it’s been sanctioned by their firms. Ignoring this fact exposes firms to adoption issues and accuracy risks. The choice is simple: meet your staff where they are with vetted AI-powered solutions or keep footing the bill for legacy platforms staff don’t want to use.

To learn even more about AI tax research adoption trends and how firms are overcoming barriers to change, you can read the full Blue J and CPA.com AI Tax Research Solution Outlook Report.

If your firm is ready to enter the AI-powered era of tax research, get started with Blue J today.

Stay up to date